Here’s Why Active ETFs Are So Hot Right Now

A constellation of factors have powered active ETFs’ meteoric rise.

Throughout the 2010s, actively managed exchange-traded funds toiled on the periphery of the ETF universe. So intertwined were passive investing and ETFs that investors needed reminders that “active ETF” is not an oxymoron.

Seemingly overnight, active ETFs ascended from obscurity to ubiquity. Their rise stems from a mixture of legislation, product development, and market events and trends that pulled their unique advantages into focus.

Taking Flight

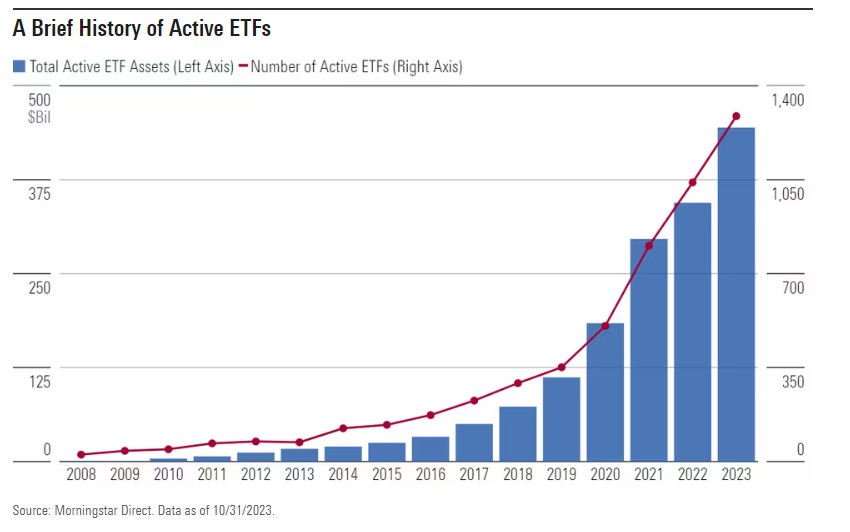

Active ETFs have exploded in recent years. In each calendar year since 2018, they reeled in at least $25 billion and notched an organic growth rate north of 30%. At the end of October 2023, they boasted $444 billion in assets—almost triple the amount from October 2020.

In the mad dash to ETFs, investors left actively managed mutual funds behind. They suffered outflows in seven of the past eight calendar years, including a record $1 trillion exodus in 2022. That seems to indicate that active management is out of style, and active ETFs have thrived strictly because they’re ETFs—boats lifted by the vehicle’s rising tide.

The ETF structure is central to the rise of active ETFs (more on that later), but they are more than fortunate beneficiaries. Active ETFs represented 3.2% of the ETF market in October 2020 but went on to claim 14% of net flows over the next three years. If active ETFs merely rode the ETF vehicle’s coattails, their market share would not have swelled to 6.3% over those three years.

Expanding the Menu

As the first exhibit shows, the number of active ETFs and their collective size have moved in lockstep. Nearly as many active ETFs launched from January 2022 through October (789) as the decade prior (810). Active ETF launches outnumbered index trackers 3 to 1 so far in 2023. The active ETF market has thrived in part because the shelves are fully stocked.

Two related developments prompted the proliferation of active ETFs. First, the SEC in 2019 approved Rule 6c-11, legislation that permitted fund providers to create and redeem ETF shares with custom baskets. This was important because it gave active managers flexibility when tapping into ETFs’ tax efficiency. Many mutual fund providers that entered the ETF market in recent years cite “the ETF Rule,” as it’s known, as the catalyst.

Motivated by the positive impacts of the ETF Rule, fund providers have found new ways to bring ETFs to the market. Converting mutual funds to ETFs has become common practice for some investment managers. Of the 1,286 active ETFs listed in October 2023, 65 started their life as mutual funds. All converted in 2021 or later.

Additionally, fund companies may soon be able to append an ETF share class to an existing mutual fund after Vanguard’s patent on that system expired in early 2023. Few shops have applied to the SEC for this capability, but proof of concept could induce more to follow and further populate the ETF market. So far, opening more lanes into it has increased traffic.

Evaluating the number of active ETFs and the flows into them can feel like a chicken-or-the-egg exercise. Did the blooming product lineup ignite more inflows, or did fund companies pounce on the vehicle’s popularity? Given how barren the active ETF cupboard was as recently as 2018—less than 300 strategies, 75% of assets in fixed-income—expanding the menu prompted inflows, not the other way around.

Unpacking the Advantages

Active ETFs’ advantages have been more obvious than their drawbacks. The unique benefits they offer have aligned with recent market events and investing trends, helping fuel active ETF adoption. Here are some pertinent examples:

Cost

Advantage: All else equal, ETFs tend to be cheaper than mutual funds. Their expense ratios strictly reflect the cost of manufacture, while mutual fund fees also embody the costs of advice, marketing, distribution, and recordkeeping. That’s why T. Rowe Price Blue Chip Growth ETF TCHP charges 14 basis points less per year than its mutual fund brethren despite their near-identical portfolios. Fourteen basis points may seem insignificant, but every dollar saved on fees is a dollar that investors can compound over time.

Impact: Investors have noted that a cost edge is a performance edge, plowing into the cheapest funds and fleeing the most expensive. The Morningstar 2022 U.S. Fund Fee Study found that the cheapest quintile of funds reeled in $394 billion, while the other 80% bled $734 billion last year, the widest disparity since 2017. Investors’ preference for cheaper funds likely pulled them toward active ETFs and their competitive prices.

Tax Efficiency

Advantage: ETFs are more tax-efficient than mutual funds. Since mutual funds deal in cash, portfolio managers frequently sell securities to generate cash to meet redemptions. This process breeds trading costs and tax bills that all fundholders absorb—even those who didn’t buy or sell. Meanwhile, ETFs tend to deal in-kind. Just the buyers or sellers bear the related costs—not the fellow investors who stand pat.

Impact: Tax efficiency is always an advantage. But after many mutual funds hit investors with the one-two punch of performance drawdowns and capital gains taxes in 2022, ETFs’ tax advantage grew all the more appealing.

Although stocks broadly plummeted in 2022, many mutual funds held appreciated securities after the long bull market leading up to it. Funds that endured outflows sold those assets to meet redemptions, saddling remaining fundholders with the taxes. For example, Vanguard Global Equity VHGEX rewarded investors who gutted out its 23% decline with a 9% capital gains distribution. Paying taxes on losing funds likely drove some investors to ETFs.

Transparency

Advantage: ETFs are more transparent than mutual funds. Most ETFs disclose their holdings daily, while mutual funds normally stick to a monthly or quarterly cadence, often with a lag. Active nontransparent ETFs report more like mutual funds, but they form a small part of the ETF market.

Impact: Transparency may matter most to financial advisors. When an individual stock goes up in smoke, their clients tend to ask: How much of this do I own? ETFs answer that question. Mutual funds may not; it could be months since they shared their holdings.

If advisors didn’t value ETFs’ transparency when stocks plummeted in 2022, there’s a chance the early-2023 Silicon Valley Bank collapse did the trick. That meltdown—confined to select stocks in one sector—prompted countless client inquiries about the specifics of their exposure.

Tradability

Advantage: Investors can trade ETFs more easily than mutual funds. Any investor with a brokerage account can invest in an ETF for the price of one share, which rarely exceeds a couple of hundred dollars. On the other hand, some mutual funds require investment minimums that investors may find prohibitive. Additionally, investors can trade ETFs at any time, while open-end fund transactions must wait until market close.

Impact: Lower investment minimums are a democratizing force, but anytime trading helps few investors. When it comes to improving investment outcomes, these perks rank well below tax efficiency and low costs.

Still, those advantages have aided active ETF adoption because they mesh well with the newest generation of investors. Charles Schwab found in a 2021 survey that 15% of all U.S. stock market investors started in 2020, and they are—on average—younger, less wealthy, and more optimistic about the market than incumbent investors. Those characteristics describe a demographic that is eager to invest but unlikely to meet the investment minimums that some mutual funds require. Accessibility mattered to the flood of investors who arrived in recent years, a consideration that likely steered them toward ETFs.

Unpacking the Disadvantages

Active ETFs have flaws. Chiefly, they cannot manage capacity by closing to new investors. Mutual funds can turn on the “no vacancy” sign when their heft starts to impede their strategies—a luxury that active ETFs do not have. ETFs are also restricted from holding certain investments. For instance, investments in private companies may add value to actively managed mutual funds but are off-limits for ETFs.

A few isolated events have pulled these drawbacks to the forefront. They weren’t as tangible or newsworthy as the events or trends that illuminated active ETFs’ benefits, though, and didn’t slow the vehicles’ torrid growth.

A New Fixture

The ETF Rule and subsequent product-development frenzy started the momentum for active ETFs, and a unique blend of market events and investing trends built on it by bringing their advantages into focus. Active ETFs are here to stay—the question is how long their dizzying rate of growth can last.